Everything You Need to Know About ACH Credit Return Reason Codes

Categories: ACH Payments

Categories: ACH Payments

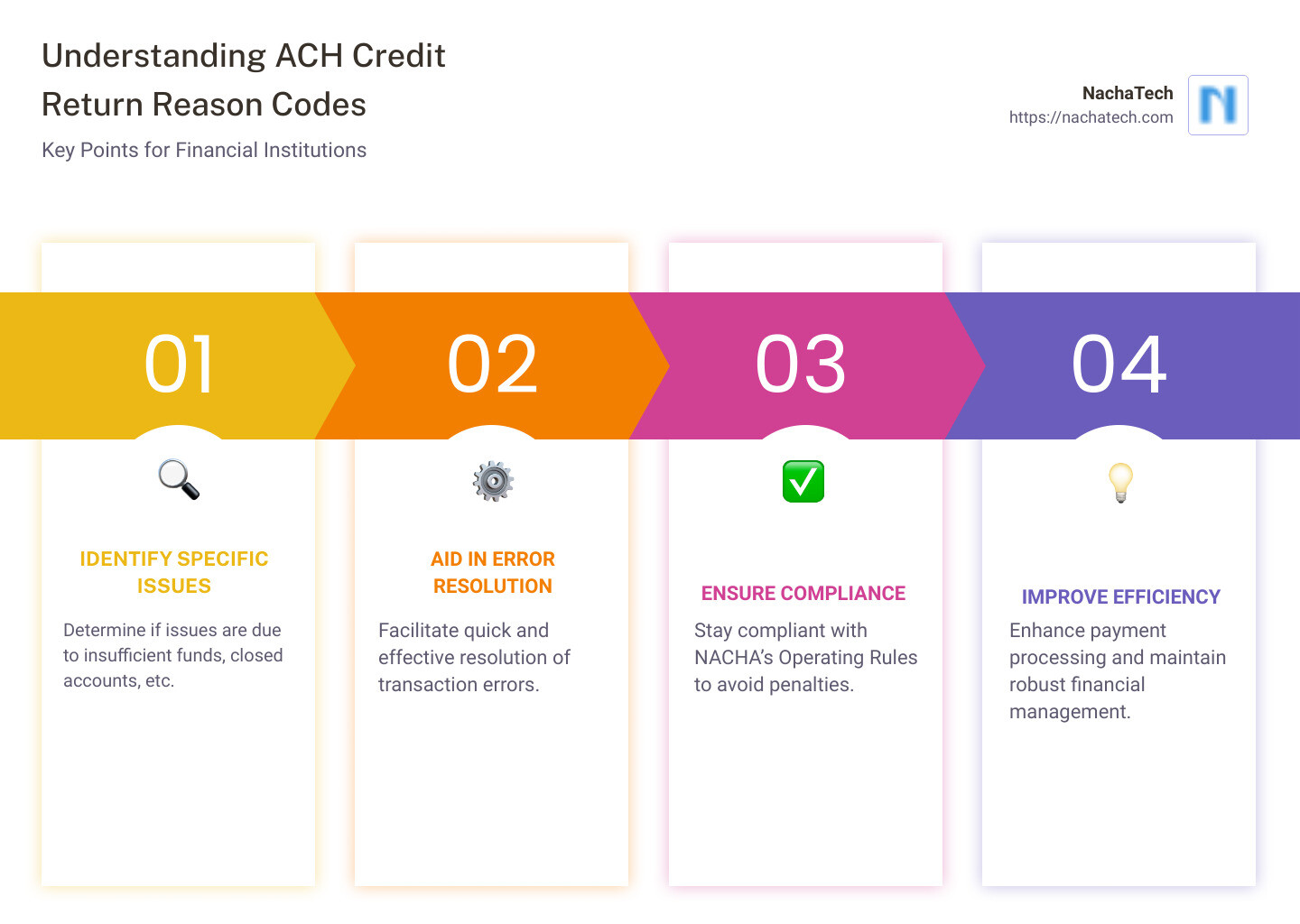

ACH credit return reason codes are vital for businesses and financial institutions to understand. These are three-digit error codes that indicate specific issues when an ACH transaction fails. Knowing these codes helps pinpoint problems quickly, allowing for faster resolution and smoother transaction processing.

Here are some quick facts about ACH credit return reason codes:

By understanding and efficiently managing these codes, financial institutions can improve payment processing, enhance customer service, reduce costs associated with returned transactions, and strengthen financial management.

ACH credit return reason codes are three-digit codes used by financial institutions to identify issues with electronic transactions. When a problem occurs during an ACH transaction, these codes help pinpoint the exact issue, guiding businesses and banks on how to resolve it.

ACH return codes are essential for error detection and resolution. They are generated by financial institutions when a transaction cannot be processed. These codes help businesses quickly identify and address problems such as incorrect account numbers or insufficient funds.

Each ACH return code corresponds to a specific error message. For example, if a transaction fails due to insufficient funds, the return code R01 will be used. This helps businesses understand why a transaction was unsuccessful and what steps to take next.

Here are some common ACH return reason codes:

| ACH Return Reason Code | Description |

|---|---|

| R01 | Insufficient funds in account |

| R02 | Account closed |

| R03 | No account on file |

| R04 | Invalid account number |

| R05 | Unauthorized debit to consumer account |

The National Automated Clearing House Association (NACHA) sets the rules for ACH transactions in the U.S. Familiarity with ACH credit return reason codes helps businesses comply with NACHA’s Operating Rules. This is crucial to avoid fines and penalties.

Example:

A business might receive an R02 return code indicating that an account is closed. In this case, the business should contact the customer to obtain updated account information before resubmitting the transaction.

Understanding ACH credit return reason codes is vital for efficient payment processing. By knowing these codes, businesses can:

By effectively using ACH credit return reason codes, businesses can ensure smoother transactions and better financial health.

Next, we’ll delve into the common ACH credit return reason codes and what they mean.

ACH credit return reason codes are essential for any business that processes electronic payments. They help you identify and fix transaction issues quickly and efficiently. Here’s why they matter:

ACH credit return reason codes pinpoint the exact problem with a transaction, like an incorrect account number or insufficient funds. This allows you to resolve issues swiftly and avoid delays.

For example, if you encounter an R01 code for insufficient funds, you can retry the transaction up to two times within 30 days. This quick action can often resolve the issue without further complications.

By recognizing patterns in ACH credit return reason codes, businesses can take preventive measures to minimize errors. This leads to smoother transactions and fewer disruptions.

For instance, consistently seeing R03 codes (No Account/Unable to Locate Account) might indicate a need to verify customer account details more thoroughly before initiating transactions.

Knowing ACH credit return reason codes helps you communicate clearly with customers about transaction issues. This transparency maintains trust and satisfaction.

Imagine a customer whose payment was returned due to an R02 code (Account Closed). By promptly informing them and requesting updated payment details, you show that you are proactive and attentive to their needs.

Familiarity with ACH credit return reason codes helps you follow NACHA’s Operating Rules, avoiding potential fines or penalties. Compliance is critical for maintaining your business’s reputation and avoiding costly errors.

Quickly resolving ACH return issues minimizes fees related to returned transactions and late payments. For example, addressing an R04 code (Invalid Account Number) immediately can save you from multiple transaction fees.

Understanding ACH credit return reason codes enables effective cash flow monitoring and helps avoid disruptions caused by unresolved transaction problems. Keeping track of these codes can highlight areas where your payment processes might need improvement.

In summary, ACH credit return reason codes are invaluable for error resolution, improving payment processing, enhancing customer service, ensuring compliance, reducing costs, and strengthening financial management.

Next, we’ll delve into the common ACH credit return reason codes and what they mean.

R01 is the most common return reason code. It means the account doesn’t have enough money to cover the transaction.

Common cause: The account holder spends more than their available balance.

How to address: You can retry the transaction up to two times within 30 days. Alternatively, contact the account holder for an alternative payment method.

R02 indicates that the account is closed.

Common cause: The account holder closed their account but didn’t update their payment information.

How to address: Contact the account holder to get their updated payment information or another form of payment.

R03 is used when the account number provided doesn’t match any existing accounts at the receiving bank.

Common cause: A typo in the account number or incorrect information given during enrollment.

How to address: Verify the correct account information with the account holder and resubmit the transaction with accurate details.

R04 means the account number entered is invalid.

Common cause: A typo or incorrect formatting of an otherwise valid number.

How to address: Correct any errors in formatting and resubmit with accurate information.

R05 is used when a consumer claims they never authorized an ACH debit transaction from their account.

Common cause: Fraudulent activity or miscommunication about authorization.

How to address: Provide proof of authorization or resolve any miscommunications with the consumer before resubmitting transactions.

R06 occurs when the originating depository financial institution (ODFI) requests a return due to incomplete, erroneous, or incorrect data.

Common cause: Clerical errors or a stop payment order by the account holder.

How to address: Review and correct any errors in the transaction or address stop payment requests before resubmitting.

R07 is used when the account holder revokes authorization for a specific ACH debit transaction.

Common cause: The account holder changes their mind and formally revokes the authorization.

How to address: Stop any future transactions based on that authorization and obtain new authorization if needed.

R08 indicates that the account holder has requested a stop payment on a specific ACH debit entry.

Common cause: Disputes, billing errors, or other reasons.

How to address: Resolve the issue with the account holder and get new authorization before resubmitting the transaction.

R09 means there are insufficient funds in the account, but the funds may become available later. It’s similar to R01 but implies a temporary hold on funds.

Common cause: Funds are held due to pending transactions or other reasons.

How to address: Retry the transaction later or contact the account holder for an alternative payment method.

R10 is used when a customer advises that the transaction was not authorized, notice was not provided, or the amount was not accurately obtained from the source document.

Common cause: Miscommunication or dispute over the transaction.

How to address: Resolve the dispute with the customer and provide proof of authorization if needed.

Understanding these common ACH credit return reason codes can help you quickly identify and resolve transaction issues, ensuring smoother payment processing and better customer service.

Next, let’s explore how to handle these return codes effectively.

Handling ACH credit return reason codes effectively is crucial to maintaining smooth payment processing and ensuring compliance. Here’s how you can manage these codes at various stages:

Error detection is the first step in managing ACH return codes. It involves identifying issues such as incorrect account numbers or insufficient funds.

Clear and prompt communication between ODFIs (Originating Depository Financial Institutions), RDFIs, and businesses is essential.

Once an error is detected and communicated, the next step is resolution.

Effective record-keeping and reporting are vital for tracking transactions and ensuring compliance.

Analyzing ACH return data is crucial for identifying areas of improvement.

By mastering these steps, you can handle ACH credit return reason codes more effectively, leading to smoother transactions and improved financial management.

Next, we’ll answer some frequently asked questions about ACH credit return reason codes.

ACH return codes are three-digit error messages used to identify issues with electronic transactions. These codes are generated when a transaction can’t be processed. They help businesses and banks pinpoint specific problems so they can be resolved quickly.

For example, R01 stands for Insufficient Funds, meaning there wasn’t enough money in the account to complete the transaction. R02 means the account has been Closed. These codes are part of the NACHA Operating Rules, which govern the ACH network.

ACH items can be returned for many reasons. Here are some common ones:

Knowing these reasons helps businesses avoid common pitfalls.

An ACH payment code is used to facilitate electronic money transfers between banks in the United States. These codes are crucial for identifying the type of transaction and ensuring it is processed correctly.

For example, ACH transactions can be either credits (money going into an account) or debits (money coming out of an account). ACH codes, such as those in the return codes list (R01-R33), help identify and resolve issues that may occur during these transactions.

Understanding these codes ensures smoother electronic payments and helps maintain compliance with NACHA rules.

Navigating ACH transactions can be complex, but understanding ACH credit return reason codes is essential for smooth and efficient payment processing. These codes help identify and resolve issues quickly, ensuring compliance with NACHA rules and maintaining the integrity of electronic payments.

At ACH Genie, we specialize in simplifying this process. Our advanced ACH file editing and validation tools are designed to minimize errors and enhance financial operations. By using our solutions, businesses can confidently manage their ACH transactions, reduce operational delays, and avoid costly mistakes.

Financial technology is rapidly evolving, and staying ahead means leveraging tools that offer precision and reliability. ACH Genie provides robust solutions that not only edit and validate ACH files but also ensure compliance with the latest regulations. This proactive approach helps businesses eliminate errors before they impact customers, fostering trust and efficiency.

In summary, understanding and managing ACH credit return reason codes is crucial for any business involved in electronic payments. With ACH Genie’s expertise and technology, you can streamline your processes, enhance operational efficiency, and ensure seamless financial transactions.

Explore more about how ACH Genie can help you manage your ACH payments effectively by visiting our ACH Payments page.

Stay informed, stay compliant, and let ACH Genie simplify your ACH transactions.